1 Dull Article About LVR Meaning & LVR Formula

Great, you’re looking for your first home and want to do research on some terms you've come across. Below are the most common questions in regards to the LVR meaning:

All these questions and many more will be answered. First, we need to understand what the meaning of LVR is.

What Is LVR meaning?

LVR stands for Loan To Value Ratio.

It is the home loan amount you’ve borrowed from the bank against the property's value. The number is then shown as a percentage. In other words, it’s the mortgage divided by the value of the property.

In the early 2000's, LVR wasn’t really a major thing. However, when house prices started skyrocketing up into the atmosphere, the Reserve Bank stepped in to implement some restrictions. One such restriction was putting in LVR limits.

With the global pandemic arriving, LVR restrictions and limits were then lifted. I’ll explain more in detail below.

How Do I calculate LVR?

Unfortunately it's a very complicated formula and will require some calculus! Just joking. The formula for LVR is below:

The LVR Formula:

Where:

- LVR is shown as a percentage

- Mortgage is technically the home loan amount you’ve borrowed from the bank

- Property Value is the market value of your property

An example of calculating LVR is as follows:

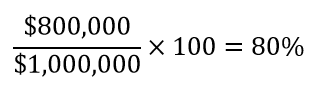

Let’s assume you’re wanting to buy a home for $1,000,000 and the deposit you have is $200,000.

- $800,000 ($1,000,000 - $200,000) is the mortgage. The amount you need to borrow from the bank

- $1,000,000 is the property value i.e. the price you paid

Plug these figures into the formula:

The above example shows an LVR of 80%. This means you’ve borrowed 80% of the value of the property, and have 20% equity in the property which was the deposit you used to purchase the property.

If you want to know more about deposits, I’ve written an article on what is the minimum deposit you will need to purchase your first home here and 8 great hacks to grow your deposit here.

This is where the legendary percentage of 20% deposit came from. Banks feel comfortable at this level lending you 80% of the value of the property as you’ve placed 20% of your own money in the property.

Why do the banks feel comfortable with 20% deposit?

With the example above, you’ve used $200,000 of your own money to buy a house. The majority of people will ensure they meet their financial obligations to the banks i.e. making sure they pay their mortgage. Because if you avoid your obligations, you could potentially lose $200,000 of the money you put in the property. Hence, why the banks will take the risk to lend 80% of the property value.

After all that, if you don’t have a calculator (I’d be surprised, there’s definitely one on your phone! haha) then you can go to this website and just plug in the numbers using their calculator.

Why do banks care about LVR?

The LVR meaning or loan to value ratio is a number that banks really look at. The two areas that banks fundamentally look at before lending money to their customers are:

- Deposit - How much money are you willing to put towards the home aka LVR

- Affordability - Can you meet the home loan repayments?

Basically, LVR means a lot to the banks as it’s their way of calculating risk. You may ask, what is the risk? The banks earn massive money from the interest on people's borrowing. Well, what happens if someone defaults (someone not being able to make their loan repayments)?

If a bank has lent a loan to a customer who only had 5% deposit (in this case, a very high LVR of 95%), the bank has put 95% of their money into that customer to buy a home. In other words, if you buy a $1,000,000 property and $50,000 is the deposit, the bank lends you $950,000.

Now compare that to someone who has 20% deposit, i.e. LVR of 80%. With the same example, the bank lends $800,000 vs $950,000. From the bank’s point of view, if a customer defaults with 5% deposit they would have lost $50,000 compared to a customer of $200,000.

The banks would rather lend that extra $150,000 from that 95% loan to another customer who has a 20% deposit, because they know the chances of getting the money returned is quite high. To them, it’s a balance between risk and reward.

What are the LVR Limits the banks will lend up to?

Banks have different LVR limits for different property types and the purpose of the property. I’ll focus on the most common ones.

Owner Occupied Property - Your Own Home

What is the LVR meaning for your own home and what is the maximum LVR limit you can go to?

As of August 2020, the majority of the banks will lend up to 80% LVR on the home you want to buy to live in. In some cases, banks will approve up to 90% and even to a maximum LVR of 95%. However, there will be an extra cost for low deposit/high LVR borrowers. I’ve written a blog on the hidden cost of buying a home with less than 20% deposit - Link here

If you’re struggling to come up with the deposit, I've also written an article for first home buyers who might be eligible to get an extra $10,000 for single and $20,000 for couple from the First Home Buyers Grant to go towards their deposit. Link here

Investment Property

As of August 2020, most of the biggest banks have recently shifted their LVR limits for investment properties. The maximum LVR is now 80%, whereas before COVID-19 hit, the maximum LVR was 70% on investment properties.

Note that each bank assesses investment properties differently, therefore some banks may still require LVR to be at 70%. Your mortgage broker will guide you through which bank is the best for investment properties for you. They’ll save you significantly more time and you want to ensure you seek great professional advice!

Property types

There are also maximum LVRs for different property types. Again, every bank has a different set of LVR rules. Here are some examples:

- Apartments with less than 45 Square metres = MAX LVR 50%

- Luxury homes = MAX LVR 70%

- Vacant land* = LVR 80%

*A note on vacant land. There are requirements, therefore best to talk to a mortgage adviser on what those requirements are as each bank is different.

Here’s a bonus one. If you’re an NZ citizen but earn foreign income and want to purchase property back in New Zealand, the maximum LVR is 70% regardless of whether you are buying your own home or an investment property.

I’ve helped many clients who are in that situation. If you want guidance and help, get in contact with me and book in a time here.

How does my Property Value influence LVR?

If we look back at the formula, the relationship between property value and LVR is significant. If the property value increases, the LVR reduces meaning it has an inverse relationship.

What this means is when LVR is low, the more equity you have in the property!

How do banks determine the value of my property?

- Registered valuation - can cost between $700-$1,200

- Purchase Price

- E-Val

- Capital Valuation (CV)

Here is an example. A couple bought their first home 4 years ago for $800,000 with a 20% deposit ($160,000). Therefore, their home loan is $640,000. Over 4 years, they’ve reduced their loan by approximately $67,000 (assuming a 30-year loan term at 3.35%).

- $573,000 is the remaining mortgage (initial loan of $640,000 - $67,000 over 4 years repayments)

- $900,000 is the property value as they got a Registered Valuation completed

Plug these figures into the formula below:

The couple has an LVR of 63.7%. What other information can you gather from this? We can work out how much equity they have. Take $900,000 - $573,000 = $327,000 which is the total equity in the house.

What can you do with all that equity?

One option is you can become a landlord and play real life monopoly.

Remember the rule for your own home, the maximum LVR is 80%. What this means is, we can only take 80% of the value of the property.

If we use the example above where the couple has $327,000 in equity, it doesn’t mean they can extract this full amount to buy their next home or use it as an deposit for an investment property.

In reality, the available equity they can use is $147,000. Not $327,000, because the banks need to hold back 20% of equity. The $147,000 is calculated by taking the value of the property and multiplying it by 80% LVR limit for owner-occupied property (home) .

$720,000 is the maximum loan amount the banks will lend you. However, you will also need to deduct the existing mortgage of $573,000 above which leaves you with the $147,000 available as equity to utilise.

If you want to learn more about investing in property, then do please contact me or book in a time with me below. Investing in property is a whole other topic, but you can see a little snippet from what I’ve already written.

Why are there LVR Restrictions?

It was back in 2010-2012 when the housing market in Auckland and other regions of New Zealand was starting to boom. Prices were spinning out of control and so the Reserve Bank of New Zealand (RBNZ) in 2013 put in some speed bumps to slow down and cool the rising property market.

This was enforced by the main retail banks i.e. ASB, ANZ etc. At the start of the boom, the maximum LVR for investment properties was 60%, so a deposit of 40% was required compared to where it is currently (20% deposit for investment properties). That significantly hampered the residential investors and implemented harsher requirements on financing too.

Over the years, the RBNZ has been adjusting LVR restrictions and most recently completely removed it. But what this LVR meaning doesn’t change the main banks internal LVR limits. At the end of the day, who are the ones lending money to us? It’s not the Reserve Bank, they set monetary policy and OCR. It’s the main banks such as ANZ, BNZ, Westpac, etc who lends us the money, so they control what those limits are. They are still in a business to make money and have to control the risk of how much they lend.

Can banks lend 100% LVR?

An option for first home buyers who are in the high LVR loan bracket is to have a guarantor in place to assist them. However, you’ll need to seek professional and legal advice to go down this path.

It's nearly impossible to buy your first home with no deposit, in fact, it is impossible. Banks want to see a minimum of 5% genuine savings from borrowers before any lending.

If you’re an investor or looking to buy your investment property, you can seek an accountant for advice on how to leverage your home to structure your loan correctly.

Summary

There you have it! It wasn't as dull as it turned out, I even gave a little value on investment properties, which is a whole other topic on its own. So hopefully you got some great value out it and I’d love to hear your feedback or if you’ve got any questions, feel free to comment below.

You can book in a time with me below and let's get you pre approved!