How To Get A Home Loan Top Up? 1 Easy Process

House prices are skyrocketing and you’re glad that you got in the market early on! As the saying goes, it’s better to be in the market now than the time the market! Pretty crazy year for NZ house prices from 2020 to the start of 2021.

Now that you’ve got a mortgage you want to get a top-up to do some renovation work around the house, given that we can’t go travelling due to COVID-19. But how to get a home loan top-up?

In this blog, I’ll share the advantages and disadvantages of having getting a top up on your mortgage. Why you should consider vs getting a personal loan.

Being adults is just juggling a whole of things at once and can get out of hand pretty quickly. For example, the car breaks down after years of driving it or something at home is broken and is quite a sizeable cost to repair it. If you haven’t got an emergency fund for these unexpected items then another option is an outlook at taking out a mortgage top up loan on your property.

How to get a home loan top up?

It’s used to be quite quick and easy to get a home loan top-up, however with the change in policy and with COVID-19 happening, most banks require basically full application when applying for any amount of top now, whether its $10,000 or $100,000.

You can either go directly to your bank to apply via online or going into the branch or see your mortgage adviser. I’d definitely recommend going to a mortgage adviser as they’ll know your situation better as he or she already has your details, secondly already understand your goals on what you want to achieve.

The first thing you need to know how much equity is in your property, as time goes on you have been paying principal and interest on your mortgage. So your loan has decreased and also if you’re lucky the property value has also increased, therefore you’ve got extra equity in the property to extract.

It all boils down to calculating the Loan to Value Ratio aka LVR. If you’re unsure what this is, I’ve written a whole topic here.

But to quickly recap it is. The formula for LVR is below:

Where:

- LVR is shown as a percentage

- Mortgage is technically the home loan amount you’ve borrowed from the bank

- Property Value is the market value of your property

An example of calculating LVR is as follows:

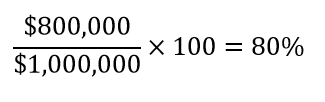

Let’s assume you’re wanting a top up of $100,000, your current mortgage is $700,000, therefore $800,000 will be the new mortgage

- $800,000. The amount you need to borrow from the bank

- $1,000,000 is the property value

Plug these figures into the formula:

The above example shows an LVR of 80%. This means you’ve borrowed 80% of the value of the property, and have 20% equity in the property which was the deposit you used to purchase the property.

If you want to know more about deposits, I’ve written an article on what is the minimum deposit you will need to purchase your first home here and 8 great hacks to grow your deposit here.

Banks will allow you to borrow a maximum of 80% of the value of the property, now this is only half the equation the other half will require you to demonstrate to the bank that you can afford this top-up.

If you’re unsure what the value of your property is, then you could use the free website such as

If you want a paid service, then you could look into Corelogic, alternatively, if you want a bespoke personal valuation, know as a registered valuation then you can ask your mortgage broker to order one, alternatively, you can do a quick google. Here is an article why you a registered valuation is required.

Once you’ve got how much equity you can extract and if it is the amount you want then you apply for the top up and most of the time the banks will require a reason why you are extracting out the equity.

So, banks will typically require the following:

- A current statement of position i.e. what is your assets and liabilities

- Current payslips

- Bank statements

- External loan statements such as car loans

- Credit card statements

Once the bank has the information or your mortgage broker, then it’ll be assessed by the bank for the approval on your top up.

When your home loan top up is approved, it is then drawn down and you can structure how you wish i.e. fix it or put in a revolving credit facility.

How does a home loan top up work?

One easy way to think of it is, you’re taking out a ‘loan’ from the property you live in. What can you do with the home loan top up? There are many options such as the following:

Consolidate debt

A lot of the time, life gets busy and we start increasing our spending without looking at our finances property. Sooner or later you’ve realised you’ve maxed out a couple of credit cards and loans. A great way is to consolidate all your debt into the top up and so you pay a significantly lower interest rate. I.e. the home loan rate current as of January 2021 is 2.29% if you have 20% deposit.

Another tip on consolidating your debt is, treat it as if you’re repaying the same amount as per the credit card and your other loans. For example, if all your loans pre-consolidation was $1,000 per week, and now the minimum repayments after consolidating is $300 per week. You still want to pay $1,000 per week!! That way you get on top of your debt as soon as possible.

Renovation works

Whether you want to upgrade your bathrooms or want to have an extra bedroom in the house to add value, you can get a mortgage top-up to get these completed. As long as you provide the bank with the extra documents and consents to do so.

Buying a car

Rather than getting finance at a dealership, having via a home loan top up will give you flexibility but similarly to consolidation tip you pay as if you were paying it over 3 years. The reason for this is life can give you curveballs. What happens during the 3 years you lose your job or you’re down to one income due to another family addition, this will give you control on your finances.

Holiday!

I know the feeling, you’re overworked and just want to have a holiday. Pre covid-19 you could easily do so just hop on a plane and go anywhere around the world. If you didn’t have the funds, people would get personal loans or just load up the credit card without considering the repercussions are when taking out loans with high interest rates. Ideally, the answer would be not to borrow money to travel.

Leverage to buy another property

If you’ve got a lot of equity you could look at buying an investment property or looking to purchase a new owner occupied the property as you can extract your equity and use it as a deposit for the next property.

I’ve written an entire article here about buying an investment property without having a deposit.

What are the disadvantages of getting a home loan top up?

- Fees and extra cost may be involved

- Borrowing for the future i.e. more debt

- Increase in repayments

What are the advantages of getting a home loan top up?

- Flexibility

- Simple and easy process for the home loan top up

- Low-interest rates

- Consolidate debt

Home loan top is not the same as home loan refinancing

I hear a lot of people talking about getting a top-up but what they are meaning is refinancing. So refinancing is elastically moving to another bank moving your mortgage from bank A to bank B.

A home loan top-up is extracting the money from the same bank you’re currently with. In other words, you’re increasing your mortgage (home loan) with your current lender.

Summary - how to get a home loan top up?

Well there you have it, hopefully, you got some value out of how to get a home loan top up.

The best way of this is actually not to get a top up at all, save your money to do those things such as

- Save money for travel

- Save money for that car, or rather buy a lower value car

- Have an emergency fund ready rather than borrow the money

Because at the end of the day you’re borrowing the money from the future and you’ll need to repay it in the future. Rather you should look at growing your wealth i.e. buying an investment property then enjoy the fruits of your labour afterwards!

If you want to learn more about investing in property or want to get a top up then book in a time with me via below with the booking system.

Alternatively, you can contact me through email will@simplyfinance.co.nz